Average True Range (ATR) as Stop and Reverse System

Order flow keeps me on the right side of the trading day. Nevertheless, I always have a chart as a guide and I keep strictly to it. The chart helps me to keep track of hectic times with the few indicators I use.

The only indicators I have installed on this chart are so-called "Non-Lagging Indicators":

VWAP, ATR, Daily Pivots and Reversal Bars. I will explain how I use them in future posts.

Today I would like to introduce how I use the ATR (Average True Range) as a guide.

In general ATR Trailing Stops are primarily used to protect capital and lock in profits on individual trades but they can also be used, in conjunction with a trend filter, to signal entries.

Average True Range ("ATR") was introduced by J. Welles Wilder in his 1978 book New Concepts In Technical Trading Systems. ATR is a measure of volatility for a stock or index. Wilder experimented with trend-following Volatility Stops using average true range. The system was subsequently modified to what is commonly known as ATR Trailing Stops.

Following is an excerpt from www.Lizardindicators.com - I am using all Indicators from Lizardindicators - about the function of ATR TrailingStop Indicator:

The ATR is a measure of volatility, disclosing the following as defined by the lookback period:

- The greatest of the current high, minus the current low

- The absolute value of the current high minus the previous close

- The absolute value of the current low minus the previous close

An average of this value is then calculated, creating the Average True Range. Of course, NinjaTrader has a predefined ATR indicator (ATR (period)). However, by using a specific formula, an ATR value based on a different input than the close, for example an average price calculation, can be applied.

Because the ATR responds to volatility, the indicator will highlight possible trend changes and may therefore also be used for stop and reverse systems. However, the ATR trailing stop is primarily suitable for defining exits, not entries [I disagree with "not entries"]. When using the ATR average as a measure for stop loss purposes, you’ll want to use a multiplication factor. We’ve set the default value to 3.5 as it allows us to accommodate more volatile instruments.

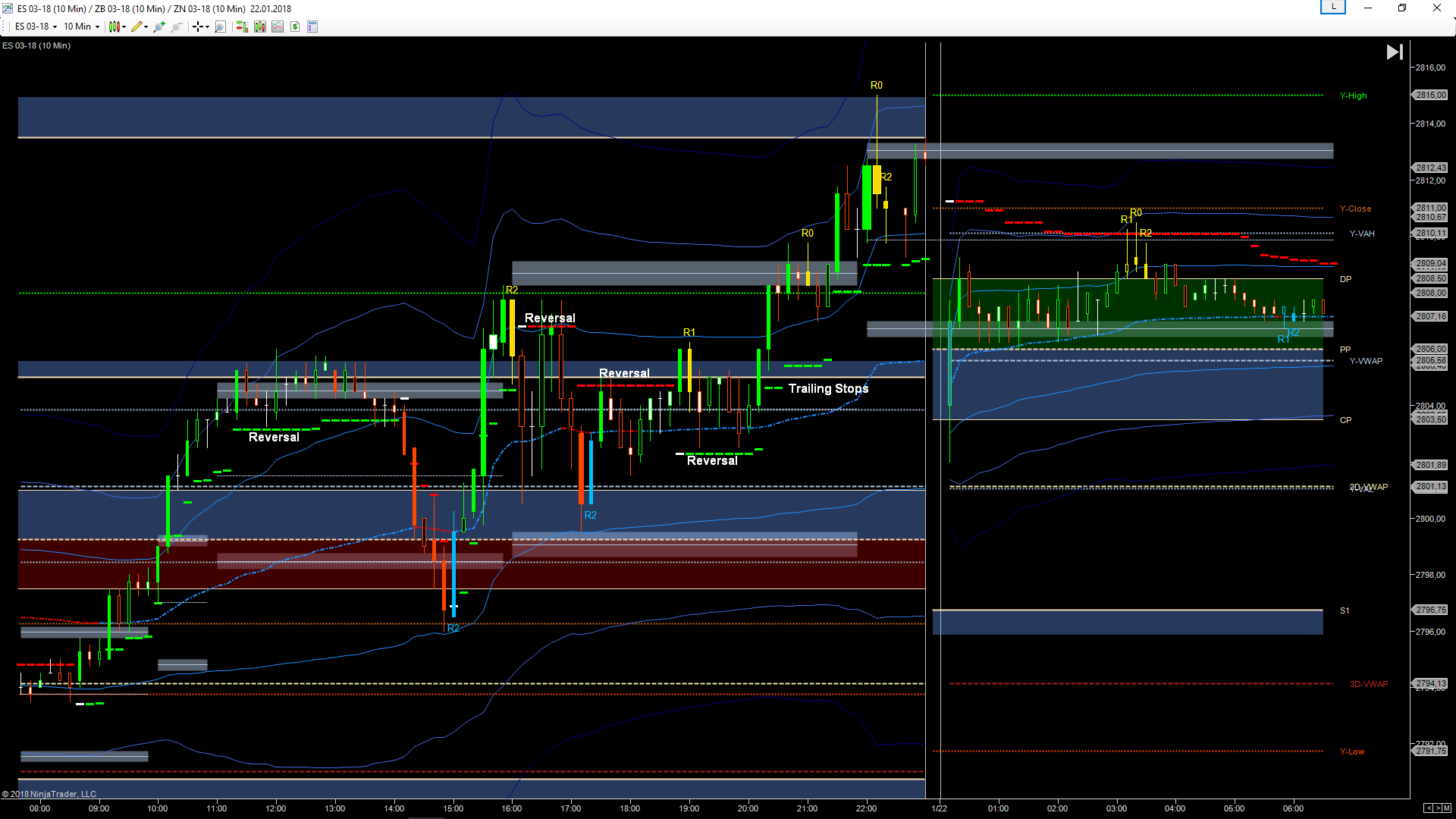

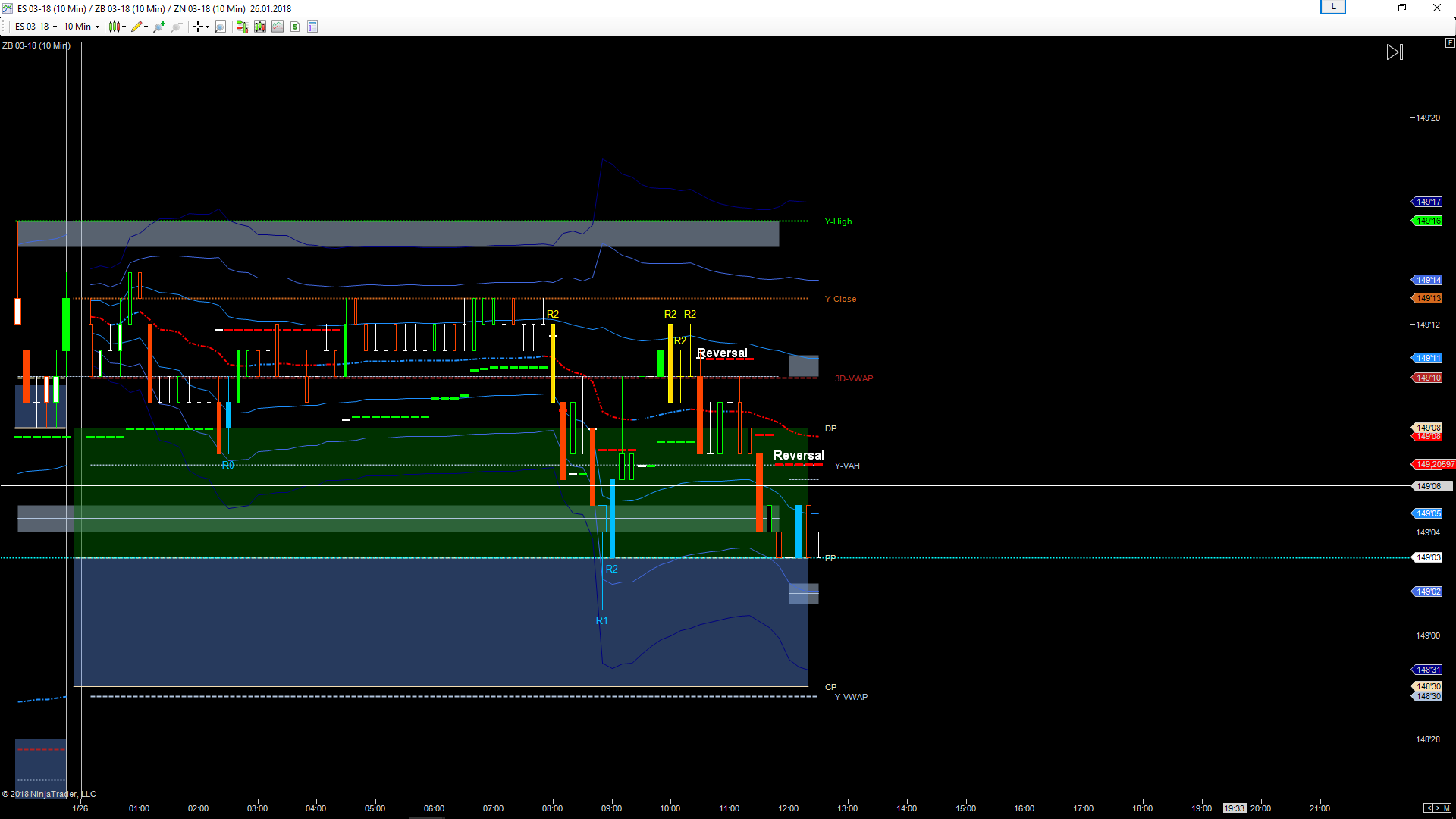

As you can see in the examples below ATR Trailing Stop can be of course used as an entry. In my experience this happens more than not. The ATR is more flexible than Fibonacci due to the "built-in" volatility calculation. Fibonaccis are fixed. By that I mean, that a 38% retracement is fixed and do not calculate actual market volatility. Yes of course, if volatility is high then the next Fibo level might be at 50% or 61,8%. But I think that ATR's adopt much better and just-in-time to daily market events.

In my observation watching Order Book like BookMap(TM) I found that around ATRs there are big limit orders placed. I don't have an explanation for that but my assumption is that others are using volatility as stop and reversal levels too.

Here some examples:

My settings are ATR Multiplier at 1,618 - 2 and ATR Period at 20.

You should make you own observations. If so, place a comment and share your thoughts.

Comments